The clarification given in Novex Communications Pvt Ltd. v. Trade Wings Hotels Limited,[i] that owners of sound recordings can issue licenses without registering as a copyright society, is significant as it has created a lot of momentum in the music licensing space in India. Various entities, engaged in the business of music licensing, came forward to seek clarifications, and started acting upon the same. One example was seen a few days ago.

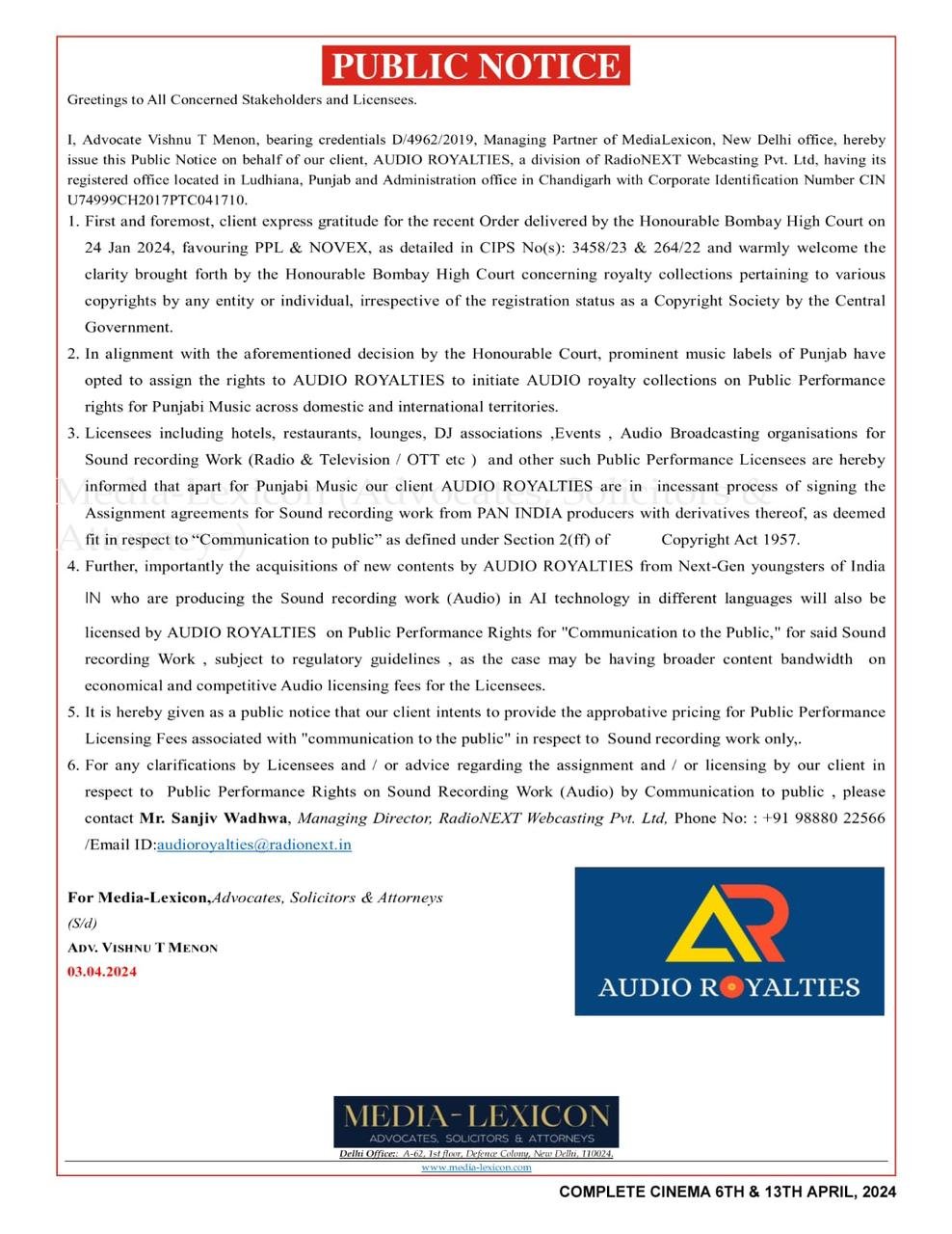

Recently, on 3rd April, a letter in the form of a public notice, was issued by an entity called ‘Audio Royalties’ to inform various music industry stakeholders, that the right of “communication to public” for its proprietary sound recordings was open to licensing.

Audio Royalties informed that music labels of Punjab have opted to assign their rights over songs to them, in order to collect public performance royalties across domestic and international territories.

The notice was aimed towards Hotels, Restaurants, lounges, DJ Associations, Events, Audio Broadcasting organisations, Radio, Television, and OTT platforms, etc., informing them that Audio Royalties can provide licenses of public performance over its catalog of “Punjabi Music”.

However, a question comes up, why was this letter even necessary?

Background

One reason could be the confusion prevalent in the music industry, partly brought about by the interpretation taken in Novex Communications v. DXC Technology Private Limited.[ii]

The Madras High Court in this case ruled that the second proviso to Section 33 (1) applied to sound recordings, and therefore, even owners could not issue licenses for sound recordings except by routing it through copyright societies.[iii]

The Court reasoned that a mischief was present prior to the Copyright Amendment Act, 2012, where authors and composers were pushed in the background, and had no share in royalties. To remedy this mischief, firstly, S. 18 and 19 were amended and authors / composers were given equal share in royalties, irrespective of any contract to the contrary. And secondly, a proviso to Section 33(1) was introduced, where issuing licenses (over underlying works or sound recordings) was restricted only through copyright societies, to ensure that royalties could be collected and shared equally with authors and composers.[iv]

This was opposite the interpretation taken earlier by Delhi High Court in Novex Communications Private Limited v. Lemon Tree Hotels Limited,[v] wherein the Court emphasized the restriction being only for musical works in the sound recording, not being on the issue of licenses over the sound recording.[vi]

Note: To put it simply, there are two components in a song, first is the lyrics, musical notes, composition, etc., (underlying works – example, the exact words which are sung) that is used to make a recording. Second is the recording itself (sound recording – the audio that you hear singing those words).

When one wants to issue license of an underlying work, as an owner, one has to do it only through a copyright society i.e., for example, IPRS.

But in Novex v. DXC it was held that even when one wants to issues license over a sound recording as an owner, one has to compulsorily do it through a copyright society.

This was not the correct interpretation in my opinion, because the intent of the second proviso to Section 33 (1) was to only restrict issuing of licenses over underlying works incorporated in a sound recording, and not the sound recording itself.

This led to some confusion in the music industry. (read more on the effect of this case prior to the Bombay High Court decision here)

Clarification

The well awaited clarification came in Novex v. Trade Wings, wherein it was held by the Bombay High Court that the right to communicate the sound recordings to the public did not fall within the second proviso of Section 33(1). This second proviso was only confined to underlying works. Therefore, the court rejected the interpretation taken in Novex v. DXC. It was also observed that no reason was provided for the decision, as to why entities issuing licenses over sound recordings would fall within the net of second proviso to Section 33(1).

Therefore, the court clarified that the second proviso would only apply to issuing licenses for underlying works, and not to sound recordings. (Read analysis of the whole judgement here)

However, the issue is still unsettled. The Delhi High Court (Novex v. Lemon Tree) and the Bombay High Court (Novex v. Trade Wings) are in favour of this interpretation. While the Madras High Court (Novex v. DXC) has ruled against it. A final clarification from the Supreme Court is now awaited.

End Notes:

[i] Novex Communications Pvt Ltd. v. Trade Wings Hotels Limited; and Phonographic Performance Ltd v. Bungalow – 9 And 99 Ors., COMMERCIAL IP SUIT NO. 264 OF 2022; and COMMERCIAL IP SUIT NO. 363 OF 2019 including others.

[ii] Novex Communications v. DXC Technology Private Limited, [2021] SCC Online MHC 6266.

[iii] Ibid, at Para 36.

[iv] Ibid.

[v] Novex Communication Pvt. Ltd. v. Lemon Tree, RFA No. 18/2019 & CM Nos. 786-789/2019.

[vi] Ibid, at Para 8.

Image generated on Dall-E

ACT, 2017 APROPOS COPYRIGHT AMENDMENT ACT, 1999 AND 2012- ONLY AN EDITORIAL REVISION")

{kind=link}

Comments are closed.